What SpaceX's Insider Trading Policy Gets Right About Employee Wealth

Srikanth Narayan

Founder and CEO

When SpaceX began trading on the Nasdaq, most of the coverage focused on valuation, Starship, and what the stock might do next.

But one section of the company's filings caught our attention—its insider trading policy.

SpaceX's policy is the first we've reviewed to include a dedicated section addressing exchange funds and diversification vehicles. The policy explicitly permits employees to participate in exchange funds, subject to pre-clearance. Even executives and directors are permitted to participate.

SpaceX's policy does something that many public companies still haven't done: it draws a clear line between speculation and diversification.

That distinction matters. For millions of employees across America whose wealth is tied to company stock, that distinction can have material consequences.

And SpaceX isn't alone.

An Emerging Best Practice

Public companies have spent years optimizing equity compensation as an incentive tool. A few are taking the lead on how they can help their employees manage the resulting risk.

A Few Companies That Explicitly Permit Diversification

These companies represent trillions of dollars in market capitalization and employ hundreds of thousands of people. Their policies share a common principle: managing concentration risk is fundamentally different from speculating on price direction.

SpaceX just validated that approach in one of the most closely watched IPOs of the decade.

Meanwhile, many company policies do not allow their employees to participate in exchange funds. In most cases, there wasn't a deliberate board-level decision on these prohibitions. General Counsels we've spoken to frequently mention that the language came from their external law firm's templates.

Concentration Risk Is a Governance Issue

If companies encourage employees to build wealth through equity, they should also consider how employees can manage the resulting concentration risk.

At Cache, we routinely meet employees whose employer stock represents 50%, 70%, or even 99% of their net worth. Most financial planners view 10%–20% of net worth as a reasonable upper bound for single-stock exposure.

Concentration grows over time. Each annual equity refresh adds to the existing pile, and a rising stock multiplies what's already there.

And here's what makes concentration risk different from most other financial risks: employees aren't simply shareholders. Their salary, bonus, career trajectory, and future earning potential are already tied to the same company. Their employer stock is only one piece of a much larger concentration.

But employees aren't positioned to influence the policies that keep them exposed. They rarely have a voice in drafting insider trading policies, even though they often bear the greatest economic consequences of those policies.

That makes this a governance question. If a company grants equity as compensation, the board should also have a considered view on how employees can prudently diversify it.

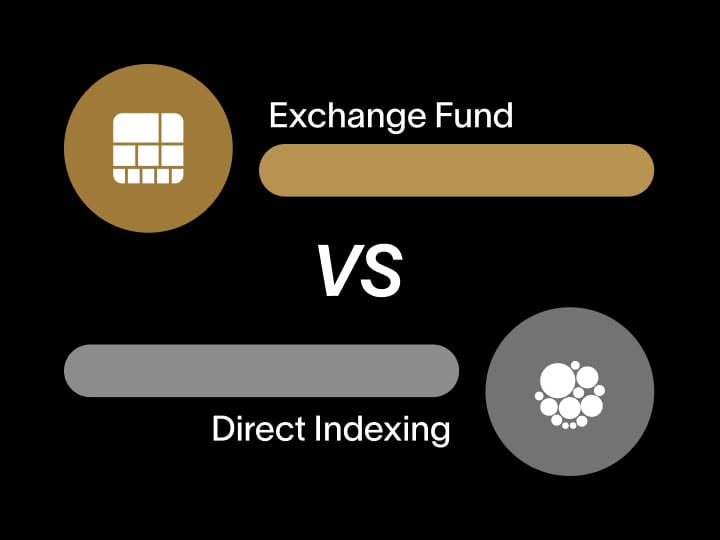

Exchange Funds Are Not Speculation

Insider trading and hedging policies exist for good reasons. They prevent behaviors that create real harms: short interest, leverage, speculative downside bets, and trading on inside information.

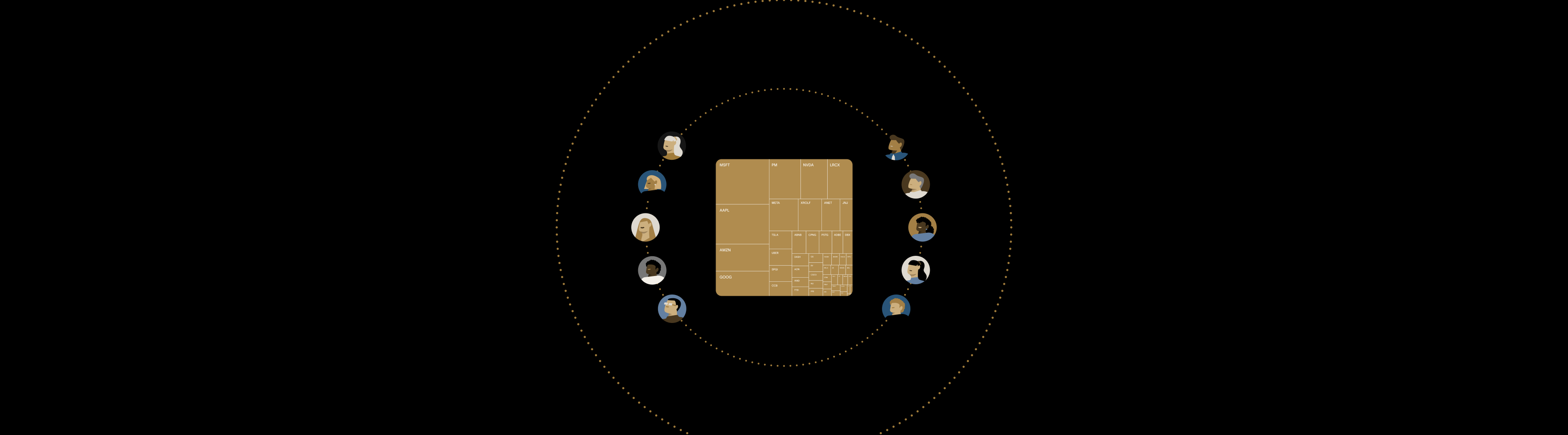

Exchange funds create none of these. An exchange fund pools appreciated stock from many investors into a diversified portfolio. Employees who contribute reduce their exposure to any single company, including their own, while remaining fully invested in the broader market. And contributions remain subject to the same pre-clearance and window restrictions as ordinary sales.

Some policies view exchange funds as hedging. Exchange funds can be structured to eliminate hedging optionality, as we've implemented at Cache.

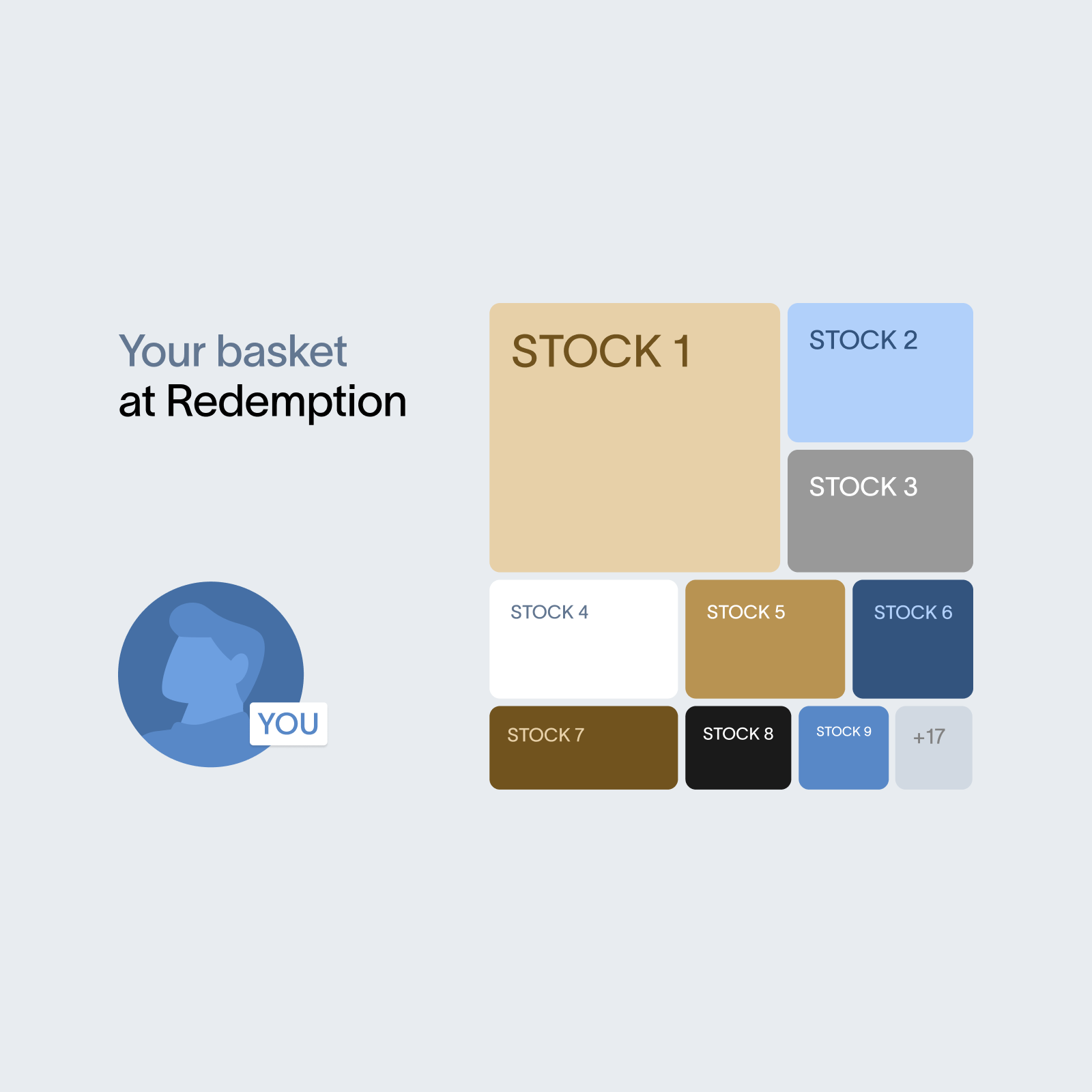

Couldn’t they just sell and reinvest during an open window? There's a simple reason many employees don’t: selling triggers a tax bill that erodes their capital base. Faced with that cost, most stay concentrated. An exchange fund achieves the same outcome without the tax friction that keeps employees stuck.

Yet many companies that are comfortable with employees selling and reinvesting prohibit them from achieving the same outcome through an exchange fund. The economic outcome is similar. The only difference is the mechanism and the tax treatment.

That distinction is hard to defend.

What the Best Policies Have in Common

The path forward is not complicated. Boards and general counsels should adopt policies that are:

Uncompromising on speculative behavior. Prohibit short sales of company stock. Prohibit speculative options or similar derivatives that profit from downside or amplify risk. Prohibit pledging or margining company stock, at least for directors, executive officers, and other key insiders.

Explicitly permissive of bona fide diversification. Allow employees, subject to standard pre-clearance and window restrictions, to participate in exchange funds and other structures where the primary economic effect is diversification, not speculation.

This is very close to what Apple, Tesla, and now SpaceX are already doing. In our view, that should become the default model for public companies.

Companies already invest heavily in employee well-being, equity compensation, and retirement benefits. A thoughtful diversification policy is a natural extension of those efforts. The goal isn't to eliminate employee ownership. It's to offer employees a way out of unnecessary concentration risk.

A Question for Boards and General Counsels

If you serve on a board, or lead legal or HR at a public company, we'd suggest one question worth raising before your next filing cycle:

Does our insider trading policy restrict employees from diversifying concentrated positions in our stock? If so, why?

If the company grants equity as compensation, the board should also have a considered view on when and how employees can prudently diversify that equity.

{{black-diversify}}

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.