Diversify your stocks. Defer your taxes.

Exchange your stock for an S&P 500 or Nasdaq-100 benchmark without triggering taxes. A time-tested strategy used by the ultra-wealthy, now available for you.

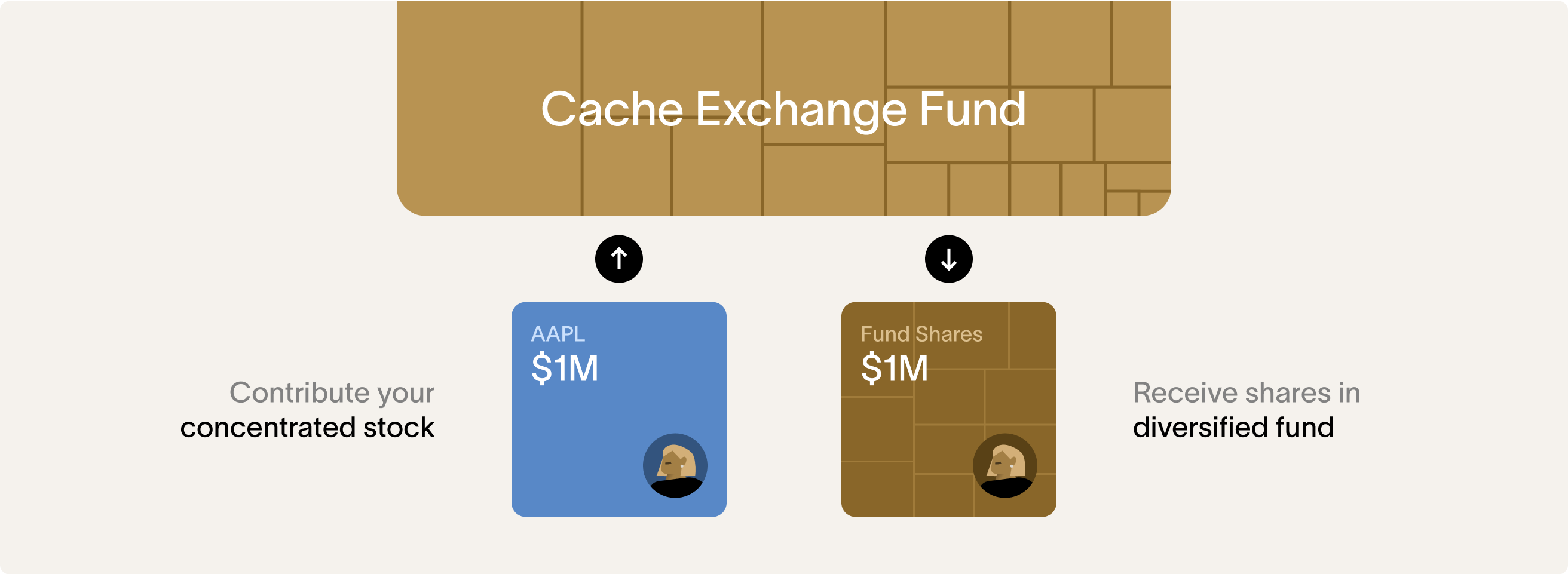

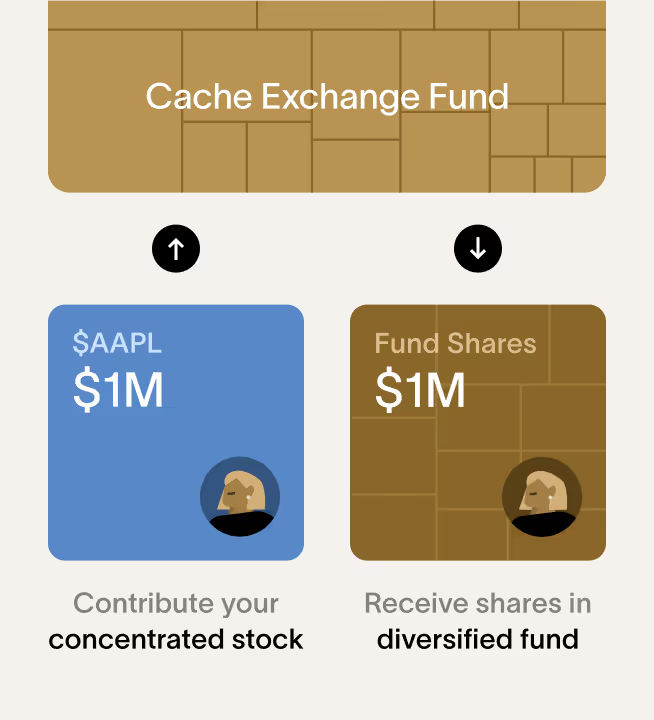

A fund you buy with your stock

Turn appreciated shares into a diversified portfolio—without selling your stock.

Put 100% of your capital to work

Contributions to an exchange fund aren’t taxable under IRC 721. Your full pre-tax value stays invested and compounding.

Diversify instantly, not over years

Tax-loss harvesting strategies can be slow or impose additional risk through leverage. An exchange fund diversifies you on day one.

Get a broad portfolio and defer taxes

After seven years, you can exchange your fund shares for a mix of ETFs and stocks, while continuing to defer your taxes.

How it works, step by step

See the impact of deferring taxes

Often misunderstood

Your money isn’t locked up for seven years

Seven years is the threshold, set by tax law, to withdraw a diversified portfolio from the fund. You can exit before seven years, and you'll receive your original stock back.

How Cache safeguards

your assets

Owned by fund investors, not Cache

Each exchange fund is owned by its investors, with Cache serving only as an advisor.

Funds held at BNY Mellon

Each fund custodies assets at BNY Mellon, the world’s largest custody bank with $50T+ in assets.

Independent admin and audit

Independent administration, accounting and annual audits ensure checks and balances.

Leaders across tech and finance have chosen Cache to diversify

Engineer at Apple

Engineer at Apple VP at Adobe

VP at Adobe Engineer at Tesla

Engineer at Tesla VP at Amazon

VP at Amazon CEO at Meta

CEO at Meta- Director at Google

- Engineer at Apple

- VP at Adobe

- Engineer at Tesla

- VP at Amazon

- CEO at Meta

- Director at Google

- Engineer at Apple

- VP at Adobe

- Engineer at Tesla

- VP at Amazon

- CEO at Meta

- Director at Google

- Engineer at Apple

- VP at Adobe

- Engineer at Tesla

- VP at Amazon

- CEO at Meta

- Director at Google

Job title and company listed is provided for illustrative purposes only to show examples of the types of investors who have invested in the fund.

Choose the fund that fits your profile

Flagship Fund Series

Our flagship funds built for Qualified Purchasers.

Tap into the engine of innovation with a technology-heavy portfolio.

Access the foundational broad market exposure across the U.S. economy.

Gain exposure to the fastest growing companies across all sectors.

Access Fund Series

Our democratizing funds built for Accredited Investors.

Gain exposure to the fastest growing companies across all sectors.

What sets Cache apart

Lower fees

0.40% - 0.95%

0.25% after seven years

No sales fee. Stock discounts.

Wholesale discounts through your advisor.

Lower fees

More than 70% higher

Sales fee: up to 1.5%

Annual fee: 0.85% - 0.95%

No tiered pricing. No stock discounts.

Lower minimums

$100K

Lower minimums

$500K - $1M

Onboarding frequency

Every two weeks

Onboarding frequency

Quarterly or semi-annually

Re-engineered for precision

Engineered to stay closer to the benchmark. Our Index Sync technology enables us with ETF rebalances to deliver predictable returns without the gaps of traditional exchange funds.

Institutional-Grade Real Estate

A thoughtful strategy to access widely diversified, high-quality real-estate portfolios with experienced managers, not individual buildings bought right before the close.

More choice at lower fees

From growth to broad market, Cache offers more fund choices for you. Your investments are aggregated across funds, lowering your effective fees. Additional discounts are available.

The Cache Advantage

The opposite of a black box

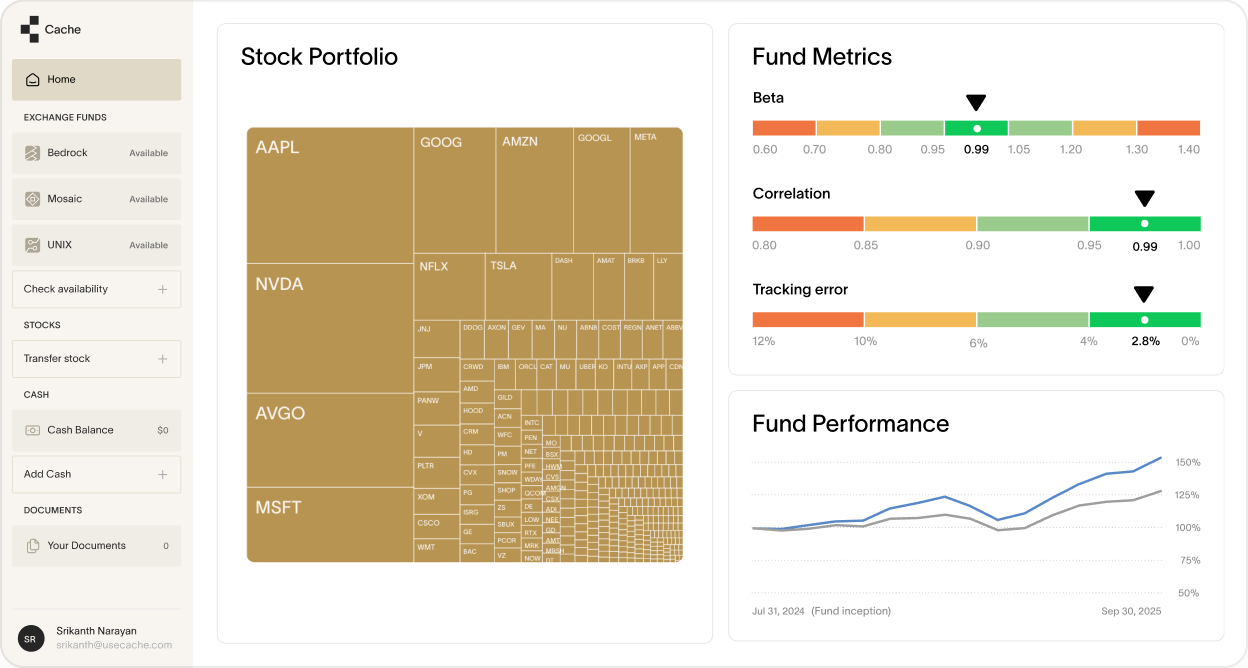

How closely it tracks

Live gauges for correlation, beta, and tracking error against your benchmark.

Returns vs. benchmark

Your fund's actual returns against the benchmark, across any time period you choose.

What's in the fund

See exactly what's in your fund: every holding, weighted by size.

Broader eligibility

Unlike traditional exchange funds, we serve both accredited investors and qualified purchasers.

Higher capacity

Our unique Index Sync structure allows for higher capacity through ETF rebalancing.

A modern experience

A digitized experience for clients and their advisors, with white-glove support along the way.

Why investors, advisors, and executives turn to Cache to diversify

"Cache solved a problem I'd been facing for years - how to diversify after over a decade of accumulating my previous company's stock without a massive tax hit. Since my first investment, I've continued to contribute additional funds, and I sleep better now knowing I'm finally diversified using a platform I trust."

"Cache brought simplicity and transparency to the exchange fund process that was traditionally complex and opaque. It made diversifying my concentrated portfolio simple."

"Cache has built THE PERFECT PRODUCT for tech professionals with concentrated stock positions — and their client service is second to none."

"Cache enables investors like our clients to eliminate single stock risk without paying a hefty diversification tax."

"The transparency in pricing and simplicity in design makes sophisticated investing straightforward and user-friendly."

"I feel great about participating in the exchange fund because I'm more in control and I'm more diversified.

"Cache solved a problem I'd been facing for years - how to diversify after over a decade of accumulating my previous company's stock without a massive tax hit. Since my first investment, I've continued to contribute additional funds, and I sleep better now knowing I'm finally diversified using a platform I trust."

"Cache brought simplicity and transparency to the exchange fund process that was traditionally complex and opaque. It made diversifying my concentrated portfolio simple."

"Cache has built THE PERFECT PRODUCT for tech professionals with concentrated stock positions — and their client service is second to none."

"Cache enables investors like our clients to eliminate single stock risk without paying a hefty diversification tax."

"The transparency in pricing and simplicity in design makes sophisticated investing straightforward and user-friendly."

"I feel great about participating in the exchange fund because I'm more in control and I'm more diversified.

"Cache provides a simple and accessible approach to diversifying post-IPO stock that many lifelong tech workers never knew existed."

"Cache made the entire investment process incredibly simple and straightforward. Not only is their product truly amazing, but the exceptional customer service makes them the absolute best in the industry. Their innovative approach sets them far ahead of competitors."

"I tried to do an exchange fund before Cache, and it was like trying to join a cult. Little info, little transparency, and little confidence with cost and charges. Cache changed all that!"

"Cache has put together an experienced, professional team that brings the tax efficient strategies of the ultra-wealthy to the masses."

"Ever since I learned about exchange funds I've been looking for something like Cache - a simple, transparent and accessible product to diversify tax efficiently."

"Cache provides a great service that just works. Their low-friction delivery of complex financial products made becoming a client an obvious choice."

"By using Cache, I felt like I made a smart decision."

"Cache provides a simple and accessible approach to diversifying post-IPO stock that many lifelong tech workers never knew existed."

"Cache made the entire investment process incredibly simple and straightforward. Not only is their product truly amazing, but the exceptional customer service makes them the absolute best in the industry. Their innovative approach sets them far ahead of competitors."

"I tried to do an exchange fund before Cache, and it was like trying to join a cult. Little info, little transparency, and little confidence with cost and charges. Cache changed all that!"

"Cache has put together an experienced, professional team that brings the tax efficient strategies of the ultra-wealthy to the masses."

"Ever since I learned about exchange funds I've been looking for something like Cache - a simple, transparent and accessible product to diversify tax efficiently."

"Cache provides a great service that just works. Their low-friction delivery of complex financial products made becoming a client an obvious choice."

"By using Cache, I felt like I made a smart decision."

Cache does not pay for testimonials or endorsements

Testimonials are provided by individuals identified as Clients above. Endorsements are provided by Advisors identified above. Advisors are not direct clients of Cache Advisors, LLC unless otherwise specified, but collaborate with Cache Advisors, LLC on behalf of their firm's clients. The testimonials and endorsements may not accurately represent the experiences of others, and there is no guarantee of future performance or success. A conflict of interest exists as the Advisors have a current business relationship with Cache. Neither Clients nor Advisors were compensated for these statements.

All you need to know

Common questions

The Basics

(X)

What's the main benefit of participating in a Cache Exchange Fund?

What are the investment goals of the Cache Exchange Fund?

Is there a taxable event after seven years? What will I receive, and what are the redemption fees?

What do you mean when you say your fund “approximates the index”?

What happens when the stock I contribute to the fund goes up or down?

How are dividends and other income treated?

What tax considerations may come up while I’m in the fund? Is there an annual K-1?

Who can participate in the Cache Exchange Fund – and which stocks are accepted?

Eligibility

(X)

How is an Exchange Fund different from an ETF?

What if I don’t meet the minimum investment amount?

May I contribute stock for a company I work at? Can I contribute unvested equity?

What happens to my cost basis over the course of the fund?

How does the real estate investment work? What happens to it after seven years?

Do you rebalance the fund quarterly, like the actual Nasdaq 100?

How are investors protected if Cache is no longer viable?

Benefits

(X)

Is the Cache Exchange Fund designed to improve my returns?

How does a Cache Exchange Fund compare to products from other providers?

How does the Exchange Fund help me avoid tax drag?

How does the Exchange Fund reduce my concentration risk?

How does Cache determine and charge fees?

How does the seven-year holding requirement compare to other providers?

Do you offer multiple funds, or is it one fund with different enrollment windows?

Getting Started

(X)

How does the reservation and formation process work?

How do you determine who gets an allocation and how big each fund is?

What happens when the fund closes?

Why do you institute a two-year lockup?

How do redemptions work before the seven-year mark? Are there any fees?

How do redemptions work once the fund “matures” after seven years? Are there any fees?

Can I transfer my shares in the fund shares or borrow against them? What are the details?

QUESTION

How is an Exchange Fund different from an ETF?

An ETF ("exchange-traded fund") is a fund that can be bought and sold on public exchanges. They typically hold a pool of stocks and/or bonds towards a particular investment objective. You can buy ETFs with your money at most brokerages.

An exchange fund is a tax-efficient private fund owned by investors who exchange their individual stock for shares in the fund. Exchange funds only accept “in-kind” stock contributions, not cash. Also, shares in the fund cannot be bought or sold on public exchanges.

The understandable confusion between “exchange fund” and “ETF” is caused by the two very different definitions of “exchange” in their respective names.

We've rethought exchange funds from the ground up, turning a mostly manually run operation into a highly precise and automated solution that’s accessible to a much larger audience.

How does a Cache Exchange Fund compare to products from other providers?

Cache makes exchange funds easier and more accessible than other providers.

Our innovative structure achieves tighter tracking to the benchmark through ETF rebalances.

Our funds break down the barriers to investing in exchange funds through lower minimums, lower eligibility criteria, and lower fees that are offered direct-to-consumer.

We also offer an intuitive and accessible experience that demystifies a previously labyrinthine financial instrument.

See if Cache Exchange Fund is right for you.

A complete

diversification toolkit

Access all the tools you need to diversify your concentrated stocks in one place.

Cost basis of your shares

For shares with significant gains and typically a low cost basis

For managing transitions from shares with moderate gains

For diversifying shares with low embedded gains