Optimizing IRA Rollovers with NUA: Turn Employer Stock into Tax Alpha

Aaron White, CFP®

Head of Investor Solutions

While most of my conversations with investors and advisors are about concentrated stock positions in taxable accounts, occasionally someone will ask about planning opportunities with retirement accounts.

The good news is that concentration risk inside a retirement account can be eliminated immediately without triggering a tax bill. Taking a distribution, however, results in taxable income at ordinary rates.

When you leave your company or reach age 59½, you can roll your 401(k) into an IRA and continue deferring taxes until required minimum distributions (RMDs) typically begin at age 73, depending on your birth year. One of the conventional planning approaches is to delay withdrawals for as long as possible. However, eventually, every dollar distributed is taxed as ordinary income, and any remaining balance at death is taxable to your heirs eventually.

But what if a portion of your retirement account could be treated differently with capital gains treatment, lifetime deferral, and a potential step-up in basis on post-distribution appreciation?

That’s where a little-known provision of the tax code comes in. Under Section 402(e)(4) of the Internal Revenue Code, employer stock held in a 401(k), ESOP, or pension plan may qualify for Net Unrealized Appreciation (NUA) treatment. This rule allows part of your retirement account to be taxed at favorable long-term capital gains rates instead of higher ordinary income rates.

If you’ve spent 20+ years at a single company, and your company allows the purchase of employee stock you may be part of a fortunate group who has a large employer stock position inside your retirement plan. In this article, we’ll explain how NUA works and who qualifies, break down the federal tax rules, and review important state-level considerations. From there, we’ll highlight how pairing NUA with exchange funds can turn concentrated stock into a diversified portfolio without losing favorable tax treatment. Finally, we’ll walk through a hypothetical Costco executive case study, comparing three retirement scenarios side by side.

NUA Explained: How Employer Stock Gets Special Tax Treatment

NUA applies to employer stock held inside a qualified retirement plan. The core idea is straightforward, but execution is governed by strict rules:

- The cost basis of employer stock is taxed immediately as ordinary income in the year of distribution.

- The NUA portion—the appreciation that accrued inside the plan—is deferred until you sell and taxed at federal long-term capital gains rates, even if sold immediately.

- Any post-distribution growth is taxed as capital gains (short- or long-term, depending on holding period after distribution).

Who Qualifies for NUA and How It Works

All conditions must be satisfied to take advantage of NUA benefits. Missing one disqualifies the treatment, additionally as this is complicated from a tax perspective we encourage you to work with a qualified tax professional.

- Triggering event: Retirement, separation from service, reaching age 59½, disability (certain plans), or death.

- Lump-sum distribution: The entire balance of that employer’s plan must be distributed in a single tax year.

- In-kind distribution: Employer stock must be transferred as shares, not sold inside the plan.

- IRA rollover for other assets: The non-NUA portion of the 401(k) plan (e.g. mutual funds, ETFs, ineligible stocks) can be rolled into an IRA.

Breaking Down the Federal Tax Rules

The table below shows how each part of employer stock is treated under NUA at the federal level:

Important Estate Planning Note: Under Rev. Rul. 75-125, Net Unrealized Appreciation (NUA) is considered income in respect of a decedent (IRD). As a result, the original NUA amount does not receive a step-up in basis at death. Only appreciation that occurs after the in-kind distribution from the retirement plan may qualify for a step-up. When sold, the original NUA portion retains its long-term capital gains character and is subject to federal and state capital gains tax, but not the 3.8% Medicare surtax.

State Tax Considerations

California is a clear example. The state allows you to defer tax on the NUA portion until the eventual sale but does not offer preferential capital gains rates. Instead, gains are taxed as ordinary income at rates up to 13.3%, the highest in the country. For high-tax states, the benefit of NUA is primarily tax deferral, and careful modeling is essential to determine net value.

Information provided for illustrative purposes only and is subject to change. Please consult with your tax advisor for information specific to your situation.

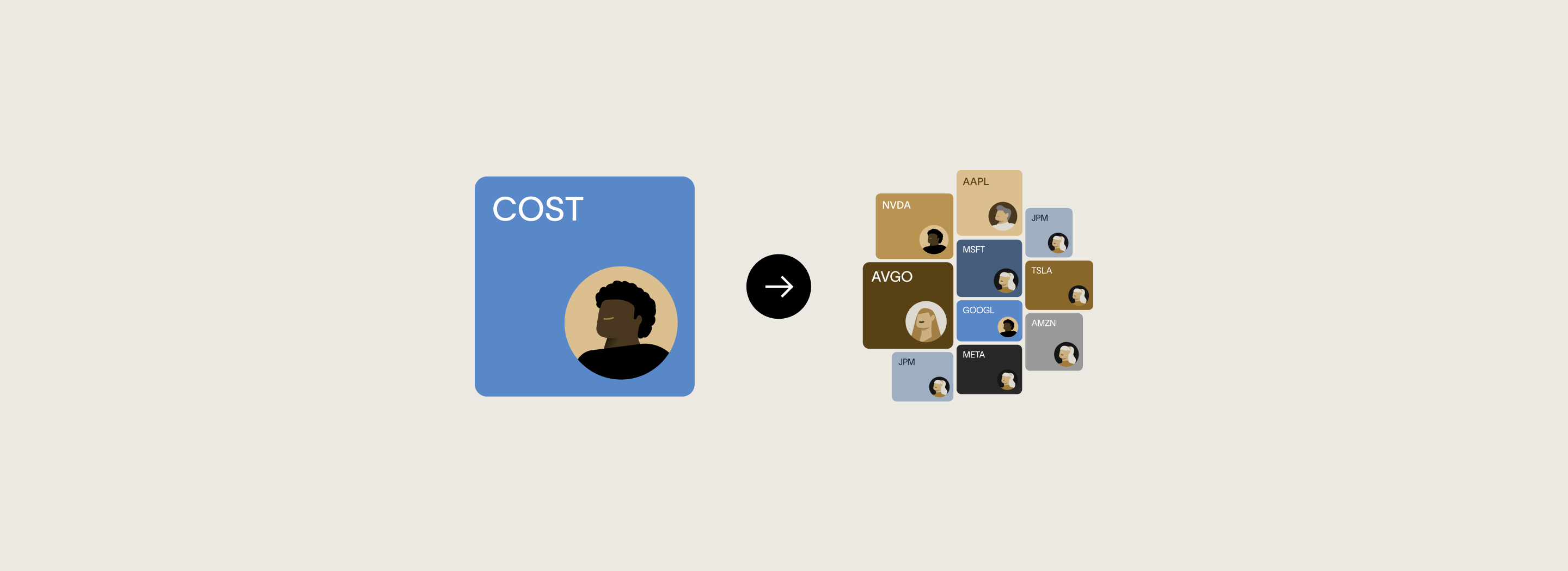

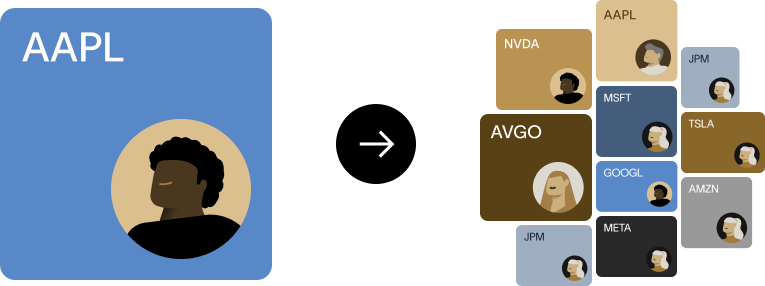

Enhancing NUA Benefits with an Exchange Fund

NUA can significantly improve federal tax treatment by converting part of your retirement account into long-term capital gains. But on its own, NUA doesn’t solve the problem of concentration risk. Exchange funds bridge that gap.

- Investors contribute appreciated stock into a pooled partnership and receive a diversified portfolio interest in return.

- Contributions are a non-recognition event under IRC §721—no tax triggered, basis carries over.

- When stock is contributed after an NUA distribution, the basis and appreciation split is preserved inside the fund.

This sequence—NUA first, exchange fund second—allows immediate diversification without losing favorable federal tax treatment, helping reduce both long-term tax costs and portfolio risk.

👉 How do exchange funds work? The ultimate guide

Case Study: Meet David, VP of Operations at Costco

David has spent more than 30 years helping his company grow and scale into the global leader it is today. Along the way, he steadily built up his retirement savings in the company’s 401(k) plan. Like many long-tenured executives, his account has grown large and heavily concentrated in Costco stock.

David is 62 years old and beginning to think about retirement. His goals are clear: he wants his retirement account to continue growing, preserve as much tax deferral as possible, and reduce his exposure to a single company’s stock. He doesn’t expect to need liquidity for at least the next 10 years, giving him the flexibility to pursue strategies that optimize for long-term tax treatment.

David’s Challenges

- Concentration risk: Over half of his retirement account is in Costco shares, leaving him exposed to a single stock’s volatility.

- Tax efficiency: Any distribution from his 401(k) is normally taxed as ordinary income, potentially creating a giant tax bill.

- Diversification: He wants to rebalance into a broader portfolio without triggering unnecessary taxes.

Planning Scenarios

David sat down with his financial advisor to map out his options. His advisor explained the Net Unrealized Appreciation (NUA) rules and how they could apply to his Costco shares. Together, they modeled three different scenarios to compare the long-term outcomes.

- Scenario A: Roll the entire balance into an IRA, deferring tax until withdrawals begin at age 73.

- Scenario B: Apply NUA to the Costco stock, move it into an exchange fund, and pay capital gains when liquidating at age 73.

- Scenario C: Apply NUA and move the Costco stock into an exchange fund. At death, only post-distribution appreciation may qualify for a step-up in basis. The original NUA remains income in respect of a decedent (IRD) and retains its capital gains character when sold.

Planning Assumptions

The analysis below is based on the following investor profile, retirement plan details, tax assumptions, and growth expectations.

Scenario Comparison

The table below compares the three scenarios step by step and shows the potential long-term impact on David’s taxes and after-tax wealth.

*IRA Distribution Rules require you to take distributions according to a standard set by the IRS called Required Minimum Distributions or RMDs.

Results

By pursuing the NUA strategy and contributing his Costco stock to an exchange fund, David can diversify immediately and preserve favorable federal tax treatment. The strategy could save him an estimated $510k after tax compared to a traditional rollover, while also reducing concentration risk. If the exchange fund qualifies for a partial step-up in basis, the benefit could grow to nearly $1.32M more than a full rollover by age 73, and even higher at full life expectancy. Note that in order to do this, the investor needs to be willing and able to make the tax payments due at the time of rollover.

Key Planning Takeaways

- ✅ NUA allows you to convert part of your 401(k) into capital gains treatment federally.

- ✅ Combining NUA with an Exchange Fund diversifies a concentrated stock position while preserving federal NUA benefits.

- ⚠️ Must follow NUA rules strictly (triggering event, lump-sum distribution, in-kind transfer).

- ⚠️ Exchange funds require longer hold periods (often 7 years) and accredited investor status.

Should You Consider an NUA Rollover?

NUA can be a powerful planning tool, but it’s not the right move for everyone. Before pursuing this strategy, it’s worth weighing the following considerations with your advisor:

- % Gain on Employer Stock: The larger the gain, the greater the potential benefit may be.

- Flexibility: Without an exchange fund, any sale after NUA triggers capital gains.

- Exchange Fund Eligibility: Not all employer stock qualifies. Funds typically require larger publicly traded stocks with daily liquidity.

- Liquidity Needs: Typically best suited for long-term holders without near-term cash needs.

- Concentration Risk Pre-Rollover: Waiting for NUA eligibility leaves you exposed to employer stock volatility.

Conclusion

NUA planning can be a powerful way to optimize retirement distributions, especially for executives or long-tenured employees with significant holdings of employer stock. By combining NUA tax treatment with an exchange fund, it may be possible to both unlock federal capital gains treatment and diversify away from concentration risk—two of the most pressing challenges facing retirement investors today.

Every situation is unique, and the rules are complex. But if you’ve built up a large position in company stock within your 401(k), the potential benefits are too significant to overlook.

Next Steps

If you’d like to explore whether an exchange fund could be the right fit for your portfolio, or a solution to bring forward in client conversations, learn more about managing concentrated stock with exchange funds:

👉 Check availability and get matched to an exchange fund

Disclaimer

This content is for educational purposes only. It is not tax, legal, or investment advice. Please consult with your CPA, attorney, and financial advisor before making any decisions.

Investment returns are not tax-free or exempt from tax liability and gains are postponed or deferred until a sale or other qualifying event results in recognition of any taxable gain. Investing in an exchange fund includes the risk of loss, including the loss of the entire principal and any rates of return that are ever illustrated are not guaranteed.

The possible effects of investment losses may impact the relative advantage of the taxable vs tax-deferred investments. Ordinary income tax rates on capital gains and dividends would affect the taxable investments return investors should consider their anticipated time horizon and income tax bracket when making an investment decision as the illustration may not reflect these factors and the assumed rate of return is not guaranteed; investment losses can reduce the relative advantage of the taxable versus the tax-deferred investments including potentially substantially which would mitigate the advantages of tax deferral. This illustration applies only to investors who reside in that state. Additional state taxes may negatively impact your performance if you reside in another state.

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.