How to reduce your capital gains taxes when selling appreciated stocks

Srikanth Narayan

Founder and CEO

Aaron White, CFP®

Head of Investor Solutions

TL;DR

- If you're sitting on a large appreciated stock position, capital gains taxes can take 20% to 37% of every dollar you realize, depending on your state and income.

- Six strategies could lower that tax bill:

- hold for long-term rates

- swap into an exchange fund

- borrow against your stock while avoiding margin risk with a prepaid variable forward

- use tax-loss harvesting through a direct-indexing or tax-aware long/short strategy

- donate appreciated shares

- claim QSBS exclusions if you qualify

- Investors find that a combination of two or three of these maybe right for them, based on your liquidity needs, time horizon, and giving plans.

Why concentrated stock holders wait too long

An appreciated stock position is a good problem until you try to sell it. The capital gains bill is what keeps most people frozen.

Maybe you're looking at a house, funding a kid's college, or just trying to stop having your net worth ride on a single ticker. Whatever the goal, the tax math feels punishing. You sell, and a third of your stock walks out the door before you've reinvested a dollar.

Another psychological trap is the price anchor. You might have a mental target for your stock, such as a prior high, a "recovery" price, or simply a round number — and wait for the stock to hit it before acting. The harsh reality is the stock may never reach that target.

This guide walks through how capital gains taxes actually work in 2026, why the tax drag matters more than the headline rate, and six strategies you can use, sometimes together, to keep more capital working for you.

How capital gains taxes on stock sales work in 2026

What is a capital gain?

A capital gain is the profit you realize when you sell an investment for more than you paid. Buy a share for $100, sell for $150, and your capital gain is $50. The government taxes that gain at preferential rates compared to ordinary income, but only if you hold the stock long enough.

When do you pay capital gains taxes?

You owe capital gains taxes only when you realize the gain. Holding an appreciated position triggers nothing. The tax bill comes due in the year you sell, and you pay it when you file the following spring.

Unlike real estate (where exchanges and primary-residence exclusions can defer or reduce gains), stocks generally trigger taxable gains every time you sell. That asymmetry is part of why concentrated stockholders get stuck.

Long-term vs short-term capital gains rates

The federal code rewards patience. Two brackets matter:

- Short-term gains apply to assets held one year or less. They're taxed at ordinary income rates, from 10% to 37% federally.

- Long-term gains apply to assets held longer than one year. They're taxed at 0%, 15%, or 20%, depending on your taxable income.

The One Big Beautiful Bill Act (OBBBA), signed in July 2025, made the long-term rate structure permanent. The thresholds adjust annually for inflation. For 2026, the 0% bracket runs up to $49,450 (single) or $98,900 (married filing jointly), and the 20% bracket kicks in above $533,400 (single) or $600,050 (married filing jointly). Anyone with taxable income above the 20% threshold pays the top rate on every additional dollar of long-term gain. (Current IRS brackets here.)

State capital gains taxes and the NIIT

Federal tax isn't the whole picture. Two more layers stack on top.

The Net Investment Income Tax (NIIT) adds 3.8% on capital gains for single filers with modified adjusted gross income above $200,000, or joint filers above $250,000. Those thresholds aren't inflation-indexed, so more people get caught by NIIT every year.

State taxes vary widely. Some states (Florida, Texas, Washington, Tennessee, Nevada) don't tax capital gains at all. Others tax them as ordinary income with no preferential rate. California is the harshest for high earners: it taxes long-term gains at up to 13.3%, no holding-period discount.

If you live in California and earn more than $1M in taxable income, your all-in long-term capital gains rate can hit 37.1%:

- Federal long-term capital gains: 20.0%

- Net Investment Income Tax: 3.8%

- California state income tax: 13.3%

- Total: 37.1%

That's the rate that drives almost every strategy below.

Many locales impose local taxes on all income. Our Capital Gains Tax Calculator can help estimate your specific number.

The hidden cost: tax drag on a concentrated position

Paying taxes today doesn't just hurt today. It compounds against you for as long as the money would have stayed invested.

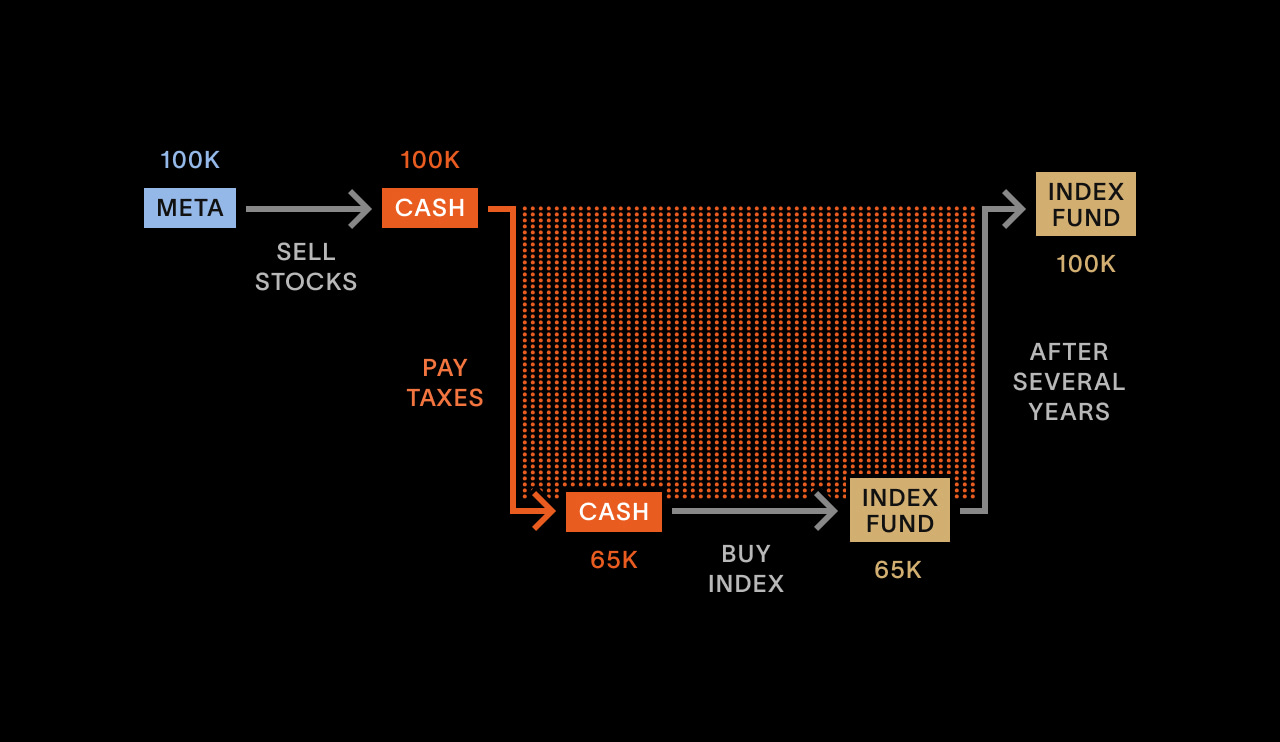

Picture an early Meta employee with $100,000 of stock at a near-zero cost basis. Selling and reinvesting in California means paying roughly $35,000 in taxes upfront, leaving $65,000 to compound. For our investor, it can take several years just to get back to where they started from. If the diversified investment returns 10% annually after expenses for 10 years and the tax rate stays the same, the investor who deferred the gain ends up with about 27% more after-tax wealth than the one who paid taxes upfront.

That gap is tax drag at work, and it's the reason sophisticated investors structure their portfolios around delaying tax realization.

Chart is illustrative, not a recommendation to buy or hold any security. Assumes a cost basis of $0, a 35% combined long-term capital gains rate.

For a real-world example of how this plays out, read Eric's story: how Cache helped protect his Tesla position as the market dropped. A traditional sale would have triggered over $388,000 in capital gains taxes for him. Deferring let him keep his full $1.12M working.

Six strategies to reduce capital gains taxes when selling stocks

Strategy 1: Wait for long-term gains

The simplest move is also the most overlooked. Short-term rates can be 15 to 20 percentage points higher than long-term rates in a high-tax state. If you vest RSUs and do not immediately sell, or you bought a stock that doubled within a year, it might be worth considering if you'd rather wait for long-term capital gains to apply.

The mechanism is straightforward. If your federal short-term rate would be 37% and your long-term rate would be 20%, the value of waiting past the one-year mark is 17 percentage points of every gain dollar. The stock would have to lose 17% of its value in that wait period to undo the benefit. In most market conditions, that's a coin flip you take.

The trade-off: a single stock carries concentration risk that a diversified portfolio doesn't. Waiting even an extra month has to measured against the risk of continuing to hold. A stock can drop a lot further than 17 percent within the span of a month.

Strategies 2 through 4 involve avoiding the sale entirely, or at least for several years.

The most powerful strategies sidestep the sale altogether. For long-term investors with appreciated positions, several structures let you diversify, raise cash, or transfer wealth without triggering the tax.

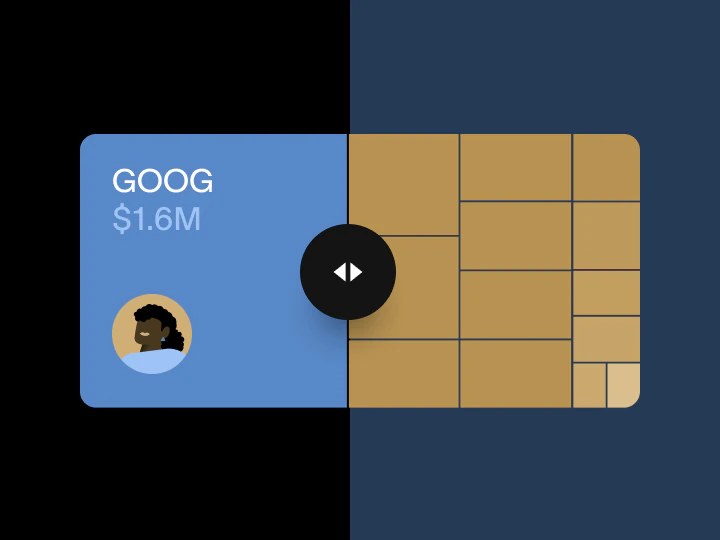

Strategy 2: Diversify immediately with an exchange fund

An exchange fund pools your appreciated stock with stock from other investors. You contribute your shares and receive a share of the diversified fund in return. No sale happens, so no capital gains are triggered. After a seven-year holding period, you can redeem a slice of the diversified portfolio — again, without any taxable event.

Time out

Is the exchange fund holding period a lockup?

The holding period is not the same as a lockup, though some exchange funds may have lockups. Cache's Flagship fund series of exchange funds (for Qualified Purchasers) does not have a fixed lock-up period — this is designed to give you additional flexibility since you can redeem earlier if needed.

Learn more by visiting our FAQ about exchange fund lockups here, and our FAQ about early redemption for exchange funds here.

*Please review offering documents for additional terms and conditions and restrictions on redemptions.

Exchange funds are typically benchmarked to a major index like the S&P 500 or Nasdaq-100. They aren't index funds, and they don't directly track an index, but they're designed to deliver performance close to the benchmark.

Until recently, exchange funds were the domain of ultra-wealthy investors with $5M-plus to contribute. Cache rebuilt the product for accredited investors and qualified purchasers starting at $100,000. Learn more on the Cache Exchange Fund product page, or see if your stock qualifies.

{{black-diversify}}

Strategy 3: Borrow against your stock

If you need liquidity but you're not ready to sell, a collar advance, also known as a prepaid variable forward, lets you borrow against most of the value of your stock and defer the sale — and your tax bill gets deferred as well.

A collar advance has three useful properties: it provides cash now, it limits downside if the stock falls, and it preserves some upside if the stock keeps appreciating (capped at a level set in the contract). At the end of the term, you may be able to roll the contract forward or let it expire and settle.

These contracts typically price well below the standard margin loans or credit lines you might be able to access. However, you should understand that these are fixed-term contracts.

Until recently, these were only available through elite private banks at $10M+ minimums. Cache has made the strategy directly accessible. Learn more about the Cache Collar Advance and get a customized quote. The Collar Advance pricing is obtained through a blind auction across numerous major banks, which is designed to ensure you receive market-competitive rates rather than a single provider's quote.

Strategy 4: Offset gains with losses

When you do need to sell, the most efficient approach is to pair capital gains with capital losses so the net taxable amount is smaller. This is called tax-loss harvesting, and it works because the tax code lets you subtract realized losses from realized gains in the same year. Unused losses carry forward indefinitely.

Two strategies help put this mechanism to work at scale.

Direct indexing

Direct indexing means owning the individual stocks that make up a benchmark index, instead of holding an ETF or mutual fund. As individual stocks in the index move up and down, you sell the losers to harvest losses, which then offset the gains you realize when selling your concentrated position.

Over time, accumulated losses let you unwind the concentrated position in tranches without paying much in taxes. The trade-off: direct indexing usually requires fresh cash to seed the strategy, since the harvested losses come from the new positions you've built up. For a side-by-side comparison of direct indexing and exchange funds, see our breakdown of direct indexing vs. exchange funds.

Tax-Aware Long/Short

Tax-Aware Long/Short takes the mechanics of direct indexing and adds a short leg and a long leg funded through margin borrowing. The strategy builds these extensions carefully, calibrated to neutralize most factor exposure relative to the benchmark.

The reason this matters: a long-only portfolio can only harvest losses when prices fall. A long/short portfolio generates tax-loss harvesting opportunities in both directions, because long positions create losses when prices fall and short positions create losses when prices rise. In a flat or trending market where direct indexing runs out of harvesting events, long/short keeps generating them.

For someone with a large appreciated position to unwind, that means the strategy can generate enough realized losses to offset the gains from selling the concentrated stock at a meaningful pace, often 10% to 20% of the position per year, depending on market conditions and leverage tier.

Long/Short is more complex and costs more than a long-only Separately Managed Account (SMA). It's appropriate for investors who can commit a meaningful portfolio to it (typically $2M+) and who want active tax-loss generation as a structural feature of their portfolio. For the full mechanics, read the complete guide to tax-aware long/short investing. If you're comparing providers, see our side-by-side of the major tax-aware long/short offerings.

Cache Tax-Aware Long/Short is sub-advised by Brooklyn Investment Group and custodied at Schwab. Try the Long/Short Tax Simulator to see how it might apply to your position.

Time out

Exchange Fund or Long/Short — or both?

Many concentrated stock positions aren't a single problem since different cost bases require different tools for tax-aware diversification. Learn the differences between exchange funds and long/short strategies, and when investors could benefit from using both →

A note on AMT for high earners: Under OBBBA, the alternative minimum tax exemption phaseout tightened for 2026. Phaseout now begins at $500,000 (single) and $1M (joint), and the phaseout rate doubled. Anyone exercising ISOs in the same year they're realizing capital gains should run the AMT math carefully with a tax advisor. AMT can dominate the strategy choice for very high earners.

Strategy 5: Get a deduction through charitable giving with a donor-advised fund

Donating appreciated stock to a Donor-Advised Fund (DAF) is one of the most efficient ways to give. You get a deduction at the stock's full market value in the year of contribution, the charity avoids capital gains entirely when the position is sold inside the fund, and you can spread the actual grants to charities over years or decades.

A DAF lets you lock in today's tax benefit while you decide later which causes to support. The contribution can continue to grow inside the fund, which means the same charitable dollar can do more by the time it lands at a nonprofit.

A note on estate planning and the step-up basis

Stocks passed to heirs at death receive a step-up in cost basis to their fair market value on the date of death. The capital gain that accrued during your lifetime is zeroed out for income tax purposes. Your heirs only pay capital gains on appreciation that happens after they inherit.

Estate taxes may still apply (the federal exemption is $15M per person starting in 2026, made permanent under OBBBA), but for many families, the step-up basis is the single most powerful tax tool available. A good estate planner can map out gifting strategies, trust structures, and the right mix for your situation.

Strategy 6: Use the QSBS exclusion if your stock qualifies

“Qualified small business stock,” or QSBS, is one of the only ways to legally exclude federal capital gains on a stock sale, but it only applies to a specific kind of stock.

If your shares are QSBS under Section 1202, you may be able to exclude all or most of your federal capital gains when you sell. QSBS applies to stock issued by a C-corporation with gross assets under a threshold at the time of issuance (the One Big Beautiful Bill Act raised that threshold to $75M for stock issued after July 4, 2025, up from the prior $50M). You generally need to hold the stock for at least five years to claim the full exclusion, and the exclusion can cover up to the greater of $15M or 10x your basis under the 2025 updates.

This is most relevant for founders, early employees of C-corp startups, and anyone who exercised options early at a venture-backed company. The rules are intricate, and state treatment varies (California doesn't conform, for example). If you might qualify, your tax advisor should be your first call before any other strategy on this list. Check out our detailed guide on how QSBS works, and how you can plan for it.

Choosing the right strategy for your situation

There's no single answer. The right approach depends on four questions:

- How big is your tax exposure?

A $200,000 unrealized gain at a 35% rate is a different problem than a $5M gain at the same rate. - How fast do you need to diversify?

Some people need to be out of a position by a specific date (an upcoming purchase, a liquidity event). Others can unwind over five to seven years. - Do you need short or mid-term liquidity?

If yes, collar advance or partial sale stays on the menu. If no, longer-term strategies like exchange funds and step-up basis become more useful. - What's your charitable or estate plan?

DAFs, gifting strategies, and the step-up basis only matter if they fit the rest of your wealth plan. And if any of your stock might qualify for the QSBS exclusion, that's a separate eligibility question worth raising with your tax advisor early.

For a quantitative starting point on the first two questions, the Cache Concentrated Stock Diversification Calculator lets you plug in your position, cost basis, and timeline to see the tax cost of different diversification paths side by side.

Thoughtful diversification plans often combine two or three strategies. A common pattern: sell some stock for immediate liquidity at long-term rates, contribute appreciated shares to a DAF to offset the gains from that sale, and put the bulk of the position into an exchange fund or long/short SMA for tax-deferred or tax-managed diversification.

A large gain is a good problem to have, and a real one at tax time. Joel's $7,000 Apple position grew past $1 million before he looked at his options. Here's the path he chose.

Cache currently manages over $1.5B for clients working through exactly these decisions. If you want a starting point, check your eligibility for a Cache Exchange Fund, or schedule a conversation with the Cache team to talk through your specific position.

Frequently asked questions

What's the federal capital gains tax rate on stocks in 2026?

Long-term capital gains (assets held more than one year) are taxed at 0%, 15%, or 20% federally, depending on taxable income. Short-term capital gains (one year or less) are taxed at ordinary income rates from 10% to 37%. The Net Investment Income Tax adds 3.8% on top for high earners.

Can you avoid capital gains tax on stocks entirely?

You can defer or eliminate capital gains taxes in several specific situations: contributing appreciated stock to an exchange fund (deferral), donating to a Donor-Advised Fund (elimination on the donated portion), holding qualified small business stock for five-plus years (Section 1202 exclusion), or passing stock to heirs at death (step-up basis). Outside these structures, you generally can't avoid the tax, only reduce it.

Do exchange funds eliminate capital gains taxes?

No. Exchange funds defer capital gains taxes. The taxes come due when you eventually sell shares of the diversified fund, calculated against your original cost basis in the contributed stock. The benefit is the deferral itself: more capital stays invested and compounds in the meantime. For the full mechanics of contribution, holding period, and redemption, see how exchange funds work.

How long do you have to hold a stock to qualify for long-term capital gains rates?

More than one year. The clock starts the day after you acquire the shares (or the day after vesting for RSUs). Selling on day 366 qualifies as long-term. Selling on day 365 still counts as short-term capital gains.

Can tax-loss harvesting offset capital gains on stocks?

Yes. Realized capital losses offset realized capital gains in the same year, dollar for dollar. If losses exceed gains, you can use up to $3,000 of the excess against ordinary income, and carry the remainder forward to future years indefinitely. Watch for wash-sale rules, which disallow losses if you repurchase the same or a substantially identical security within 30 days of a sale. For an in-depth look at how strategies like long/short generate harvestable losses systematically, see our tax-aware long/short investing guide.

What's the difference between an exchange fund and tax-aware long/short?

An exchange fund pools your appreciated stock with other investors' stock into a diversified fund. There's no taxable sale at contribution, and you hold the fund shares for seven years before redeeming. Tax-aware long/short is a separately managed account that holds long and short positions in index constituents, generating realized losses you use to offset the gains from selling your concentrated stock. The exchange fund defers taxes through a non-sale contribution. Long/short manages them through offsetting losses against an unwind. Compare exchange funds vs. long/short strategies here.

Can I contribute to an exchange fund over time instead of all at once?

Exchange funds may accept contributions across multiple closes. Cache’s Exchange Fund typically closes every two weeks, so you could spread your entry over months or years rather than committing everything at once.

This is a common way for investors with multi-million single stock positions to dollar cost average into an exchange fund. It can be a popular option for positions that have historically had short term high volatility in their stock holding or if an exchange fund doesn’t have capacity for the full position at once.

Another practical implication: contributing to different funds over time (for example, a NASDAQ fund one year and an S&P 500 fund the next) keeps your timelines distinct and gives you benchmark diversification on top of stock diversification.

Please note that each contribution will have it's own 7 year holding period.

What is an exchange fund vs. an ETF?

An ETF, or exchange-traded fund, is a publicly traded fund that holds a basket of securities — typically tracking an index like the S&P 500. You can buy and sell ETF shares on a stock exchange at any time, just like a stock. An exchange fund is a private partnership that lets you contribute appreciated stock to a diversified pool without triggering a taxable sale.

The key difference for concentrated stockholders: selling your appreciated stock to buy an ETF still triggers a capital gains tax bill on the full gain. The ETF is often used to solve the diversification problem but not the tax problem.

An exchange fund is designed to solves both — you contribute the stock directly, no sale happens, and no capital gains are triggered at the time of contribution. The trade-off is that exchange funds require a seven-year holding period, typically has higher fees, and are only available to accredited investors, whereas ETFs are available to anyone and are fully liquid.

Next steps

If your position is over $100,000 in a single stock, the strategies in this guide can save meaningful capital. Run your position through the Concentrated Stock Diversification Calculator

{{black-diversify}}

Cache Securities is a broker-dealer registered with the SEC and is a member of FINRA and SIPC. Cache Advisors is an investment adviser registered with the SEC. Registration does not imply a certain level of skill or training. Cache Advisors and Cache Securities are wholly-owned subsidiaries of Cache Financials, Inc.

To complete a purchase, an investor must complete and execute a subscription document. Any product discussed within should only be purchased after the client reviews the offering documents and executes a subscription agreement. Cache does not make investment recommendations. Investors are responsible for their investment decisions and should carefully consider the risks associated with the investment.

The Cache Exchange Funds are alternative investments. Regulations require certain eligibility criteria and are open to accredited investors or qualified purchasers as specified in the offering documents. Exchange funds are appropriate for eligible, long-term investors willing to forego liquidity and put capital at risk for substantial periods. Regulations require a minimum holding period to realize potential advantages. Exchange funds may have higher fees than traditional investments. Diversification may help spread risk but does not assure a profit or protect against loss. Exchange Funds defer taxation on investments; they do not eliminate the need to pay taxes on the sale of assets.

Collar Advance relies on a fixed-term options contract that may be difficult to unwind in volatile markets. Investors may face potential losses when trying to prematurely exit contracts, particularly during unfavorable market conditions. Although Collar Advance offers certain downside protections, investors may still face losses if share prices decline. Investors also risk foregoing gains beyond the cap levels set in the contracts. Cache Securities LLC offers the service in partnership with Fort Point Capital Partners LLC and Uhlmann Price Securities.

Cache Tax-Aware Long/Short is offered through Cache Advisors LLC and sub-advised by Brooklyn Investment Group. Accounts are custodied at Charles Schwab. The strategy involves long and short positions and may be more complex and carry different risks than traditional long-only investments, including higher fees, leverage, and tracking error to the benchmark index. Past performance is not indicative of future results. Any historical ranges referenced are estimates and should not be relied upon as indicative of future results.

Tax laws are complex and change. Cache provides information for educational purposes only. This article is not investment, tax, or legal advice. Consult your own tax and legal advisors before acting on any strategy discussed.

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.