To sell or not to sell (your RSUs)? Consider these key factors.

Srikanth Narayan

Founder and CEO

Editor’s Note: EquityFTW consulted on the creation of this article. We highly recommend their blog as a resource for managing stock compensation effectively.

A large part of your compensation is in your employer’s stock. You’re not alone—more than 80% of publicly traded companies offer stock compensation to their employees. Now the question is, what should you do with your Restricted Stock Units (RSUs) once they vest?

In my time at Alphabet and Uber, I noticed two distinct camps: some employees sold everything immediately upon vest, and others sold none at all. Internet wisdom suggests selling right away, as relying heavily on a single company for both your portfolio and income can add substantial risk. However, at Cache, we think the right answer isn’t binary. No two people have the same financial situation, so what’s worked for MemeLord72 on Reddit may not be the right thing for you.

Consider this: an employee who continuously sold their Nvidia shares on vest is likely to be kicking themselves today. At the same time, there’s a popular story about a company where employees held 30% of the outstanding stock. That company is Lehman Brothers, and its abrupt bankruptcy wiped out billions in wealth for its employees.

These stories highlight the risks of an all-or-nothing approach. Without a crystal ball, the best move lies somewhere in the middle—a thoughtful balance that aligns with your unique financial goals and comfort level. So, how can you make the most of your RSUs while managing risk? Let’s dive into practical steps to help you build a strategy that fits your financial plans.

Shouldn’t you just sell RSUs immediately?

There are several competing factors to consider, and while we’ll outline a helpful framework, it’s important to first recognize the interests you’re balancing when deciding how much of your RSUs to hold or sell:

1) Do you need the money right now?

When RSUs vest, the shares you receive are taxed just as if you are receiving cash of the exact same value. So, if you were to receive cash instead of RSUs, would you choose to invest it all in your company’s stock? And do you have any other pressing financial needs – like paying off debt, making a down payment, or paying for college?

EquityFTW put together a good article to help you understand potential tax implications – including the possibility that default withholding won’t cover your tax burden – but if you need the liquidity in the short term, you should probably sell more than you hold.

2) Are you exposed to concentration risk?

If your company’s stock makes up less than 10% of your net worth and you’re optimistic about its future, it may not be a very risky bet to accumulate more stock. In fact, you may want to accumulate more company stock to make sure you enjoy a good run.

However, if your portfolio is already concentrated in company stock, a decline in its price could have a major impact on your financial outlook. Worse, if the company faces financial issues, you could lose your salary and the value held in stocks.

Even when things look promising, the future is never certain. In many cases, it may be wiser—and safer—to diversify your holdings, even if it means missing out on some potential gains.

{{black-diversify}}

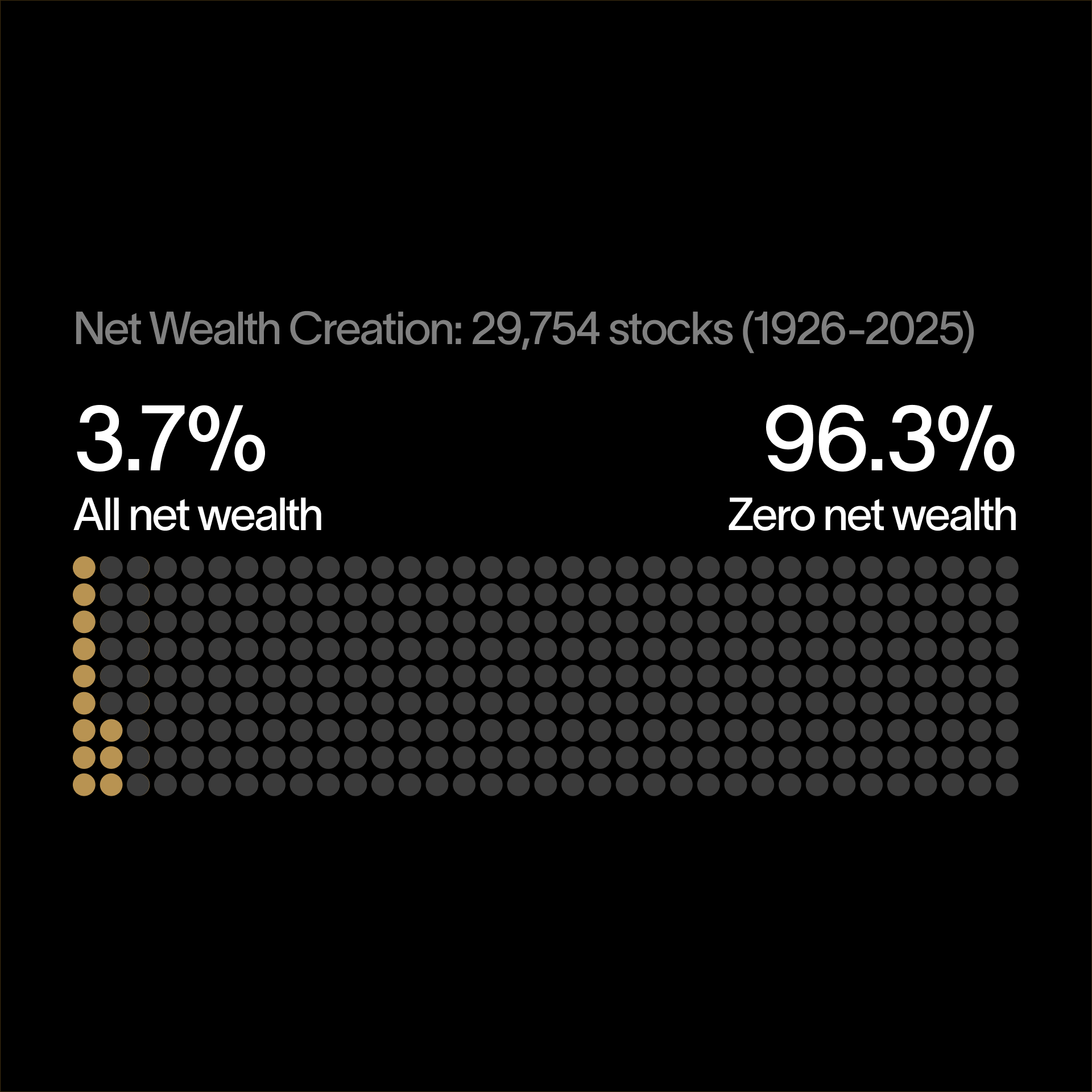

Some employees with RSUs prefer to put all their eggs in one basket – and places like Reddit’s WallStreetBets certainly contain many examples of investors who have been successful with these “Yolo” or “Diamond Hands” strategies. Over the long term, however, broad market indices have tended to outperform most individual stocks, and you are likely to earn a better return on a risk-adjusted basis. For example:

History doesn’t necessarily dictate the future, but you should definitely understand the risk you’re exposing yourself to if you become concentrated in your company’s stock. Our detailed concentration risk article takes a closer look at the potential risks and rewards of concentrated positions.

3) When are you allowed to sell?

You’re probably restricted from selling shares during certain windows. If your RSUs vest when the window is closed, you may not be able to sell immediately. And you might have accrued capital gains or losses by the time the trading windows open. It's important to keep a close eye, and optimize the lots you dispose for tax efficiency.

4) What does your gut say?

Once you’ve weighed all the logical and practical factors, it’s worth checking in with your own aspirations. Do you believe your company’s value will grow significantly in the future? And even if your instincts tell you to hold a large position, consider how concentrated you’re comfortable being.

Deciding what to do with vested equity is rarely just a math problem. Jonathan spent nearly a decade at Microsoft and took a sabbatical to weigh his options before he diversified. Here's what he decided.

Many employees and company insiders—including CEOs, CFOs, and board members—remain optimistic about their company’s future yet still take some risk off the table to manage their concentrated stock positions.

If you’re with the right company, holding on could mean striking gold, with potentially much higher returns than a diversified approach. But if things go south, being overly concentrated can be a serious financial setback. For every Tesla, Nvidia, or AMD employee who turned their RSUs into a fortune, there are others—at companies like Dropbox, Cisco, or Snowflake—whose stock has underperformed the market.

Ultimately, only you can decide how much risk feels right for you.

How to “sell” the stock from your RSUs

When it’s time to liquidate or diversify your shares, simply placing a sell order with your brokerage may not be the optimal way to move forward. For tax purposes, you should pay close attention to which shares you sell, and you may want to consider alternatives to an outright sale.

Looking at cost basis

When you sell your stocks, more highly appreciated shares – which are commonly the ones you’ve been holding the longest – will have a lower cost basis. Thus, selling them will lead to a higher tax bill, leaving you with less principal to reinvest.

This cost of diversification is called tax drag:

This image assumes a 35% effective capital gains tax rate when selling appreciated META stock to reduce concentration risk. At a 10% annual return, it would take almost five years for a diversified portfolio to recoup the taxes that were paid.

You can avoid some tax drag by selling shares with a higher cost basis first. For a stock that has been going up in value, that usually means selling the shares that have vested most recently.

To identify the best tax lots to sell, it may help to talk to an accountant or a financial advisor.

Alternatives to selling RSUs

The sale of stocks triggers a taxable event, but there are a few ways to diversify or gain liquidity without a sale. Here are a few options to consider:

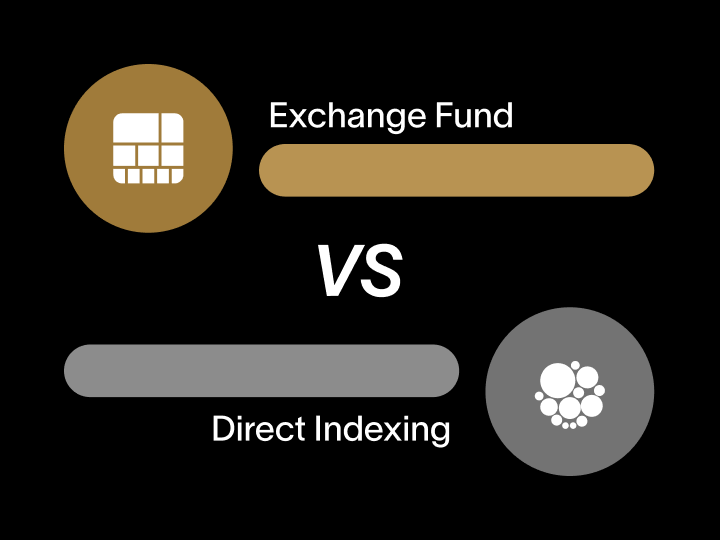

- Exchange funds: Diversify and defer taxes by swapping your stocks for a share of a diversified exchange fund. You’ll reduce concentration risk immediately. And after seven years, you can withdraw a diversified basket of stocks from the fund. No capital gains taxes are due until you decide to sell. See how it works with an exchange fund simulator.

- Collar advance: Also known as a prepaid variable forward contract, this strategy lets you borrow against the value of your shares at relatively low rates, with in-built protection against stock value declines. You unlock cash for major purchases while hanging onto your shares.

- Direct indexing: After purchasing a basket of stocks that resembles a diversified index fund (instead of ETF or mutual fund shares), you’re able to offset the gains in your stocks each time a loss is recognized in the portfolio. Over time, you’ll be able to diversify out of a concentrated position while offsetting some of the tax burden.

- Charitable vehicles: Donor Advised Funds (DAF) and Charitable Remainder Trusts (CRT) both involve donating concentrated stock to charities, but they can be structured to let you unlock the value of appreciated assets during your lifetime.

These strategies are all for sophisticated investors, but you may want to explore them if you’re looking for a better way to manage your vesting RSUs.

So, to sell or not to sell your RSUs?

The decision is ultimately yours, but we hope this framework—and a few alternative strategies to selling—has provided valuable guidance. Managing your RSUs wisely has the potential to add hundreds of thousands, or even millions, to your portfolio, so it’s fantastic that you’re approaching it thoughtfully.

<div class="blog_disclosures-text text-weight-semibold">Material presented in this article is gathered from sources that we believe to be reliable. We do not guarantee the accuracy of the information it contains. This article may not be a complete discussion of all material facts and risks. All content is for general informational purposes only and does not take into account your individual circumstances, financial situation, or your specific needs, nor does it present a personalized recommendation to you. It is not intended to provide legal, accounting, tax or investment advice. Cache does not make investment recommendations; investors are responsible for their own investment decisions. Diversification seeks to reduce risk by spreading risk across multiple investments however, Investing involves risk, including the loss of principal.</div>

<div class="blog_disclosures-text text-weight-semibold">Securities are offered through Cache Securities LLC, FINRA/SIPC. Investment advisory services are offered through Cache Advisors LLC, an SEC-registered investment advisor. Cache Advisors and Cache Securities are wholly-owned subsidiaries of Cache Financials Inc “Cache” Cache and EquityFTW are unaffiliated entities. More details about how Exchange Funds work, including the risks and benefits associated with them, is available at: https://usecache.com/product/exchange-funds</div>

{{black-diversify}}

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.