Direct Indexing in 2026: Basics, Tradeoffs, and Comparisons

A study found that only 2% of U.S. stocks accounted for over 90% of the market’s net gains from 1926 to 2022 (Bessembinder, 2023). That means the odds of picking a long-term winner are far lower than most investors think, and the risk of betting big on the wrong name is far higher. Even serious investors face the challenge that concentrated bets rarely outperform the market over time.

To get exposure to the best-performing stocks, a widely prescribed method is index investing. Buy a low-cost index ETF, and instantly own the entire market. This has been the trend that has shaped the investment industry for the past few decades, and active stock picking has lost ground to low-cost index investing.

More recently, direct indexing has gained traction among high-net-worth investors as an alternative to ETFs for index investing. Direct indexing offers more control, greater tax flexibility, and portfolios that allow for strategic modifications to reflect their views.

It’s not a silver bullet, and it’s not for everyone, but in the right situations, it can be powerful. And when paired with other advanced strategies, it can be even more effective.

What is Direct Indexing?

Direct indexing involves creating a portfolio that replicates the holdings of a specific market index, such as the S&P 500 or the Russell 1000, by directly purchasing the individual stocks that comprise that index. Rather than buying shares in an ETF or mutual fund, direct indexing provides you with precise control over each stock holding, allowing you to mirror the index's composition or make tweaks accommodating to your preferences.

It sounds complex. So, why would anyone bother? This control enables two key advantages:

- Strategic tax-loss harvesting — selling losing positions to offset gains elsewhere, then reinvesting to stay in line with your target index.

- Personalization — excluding certain companies or overweighting others based on conviction or risk profile.

Advantages of Direct Indexing

Strategic Tax Optimization

Selling underperforming stocks to realize losses can reduce taxable gains from other investments.

In high-volatility years, Morgan Stanley research estimates that disciplined harvesting can add roughly 0.3% to 1.0% to after-tax returns annually — compounding to meaningful gains over time — although results vary with market conditions, tax rates, and portfolio size.

Stock-Level Customization

Unlike ETFs, direct indexing lets you control exposure at the company level — avoiding businesses you don’t want to own, or tilting toward sectors where you see opportunity.

Drawbacks of Direct Indexing

Complexity and Oversight

Matching an index requires rebalancing, tracking dividends, and harvesting losses — tasks that demand expertise and experience. When choosing a direct indexing provider, be sure to analyze these key technical details:

- Tracking error:

This is the gap between your portfolio’s performance and the benchmark index. Aggressive tax-loss harvesting can increase tracking error if replacement stocks behave differently from harvested stocks. The smaller your portfolio or the more exclusions you make, the more this gap can grow. - Wash-sale management:

U.S. tax rules disallow a loss on a stock if you repurchase it (or a “substantially identical” security) within 30 days before or after the sale. Mismanagement can result in unexpected tax bills, whereas aggressive loss harvesting can force you to sit out on a long list of stocks.

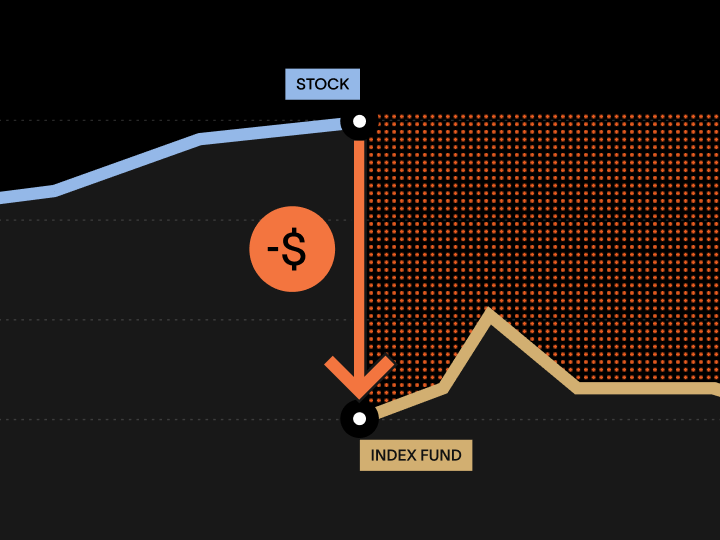

Tax Costs on Initial Setup

Direct indexing can trigger substantial capital gains taxes if investors are advised to liquidate their highly appreciated concentrated portfolio to move into a direct index, offsetting the long-term benefit. Funding the strategy with cash from earned income or a liquidity event is a better option, when deferral options are no longer available.

Portfolio Lock-In

The value of direct indexing often comes from harvesting losses to offset gains. Over time, especially in prolonged bull markets, portfolios can “ossify”, or become locked in, as most positions move into large unrealized gains. Once this happens, annual loss-harvesting opportunities may be too small to justify the ongoing complexity and costs.

If your direct indexing portfolio has locked in, a tax-aware long/short strategy can refresh your loss-generating capacity without changing your net market exposure. Unlike direct indexing, long/short continuously creates new loss opportunities even in rising markets.

👉 See your after-tax projection with long/short

Direct Indexing vs. Low-Cost ETFs

For many high-net-worth investors, the natural question is: Why not just buy a low-cost index ETF and hold forever? Or, should I transition my ETF portfolio into a direct index?

ETFs are, by design, extremely tax-efficient:

- They use in-kind redemption mechanisms to avoid recognizing or distributing most capital gains.

- As the index composition changes, ETFs can rebalance with no tax consequences.

- Many broad-market ETFs go years without a taxable gain payout.

When sticking with ETFs may make sense:

- You already hold highly appreciated ETF shares, and selling them to move into a direct index would trigger immediate gains.

- You value simplicity, and the complexity of tax reporting or the stock-level customizations does not appeal to you.

When a direct index may be able to add value:

- You have a portfolio of assets that regularly generate capital gains (e.g., hedge funds, actively managed mutual funds) and want to harvest losses elsewhere to offset them.

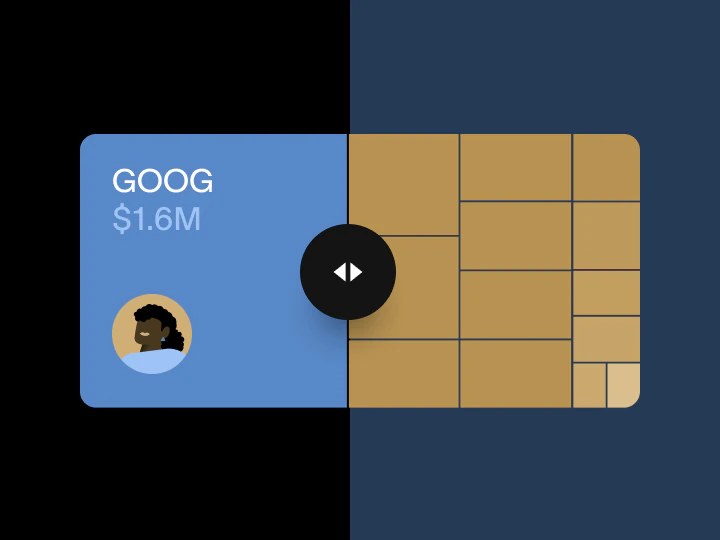

- You hold a large single-stock or other appreciated asset and want to gradually diversify into index-like exposure while chipping away at the tax impact over time.

- You want the flexibility to exclude certain companies or overweight others while still closely tracking a benchmark.

- You’re in a high tax bracket and have enough capital to make ongoing harvesting meaningful.

Where Exchange Funds Fit

Direct indexing works well for diversified taxable portfolios, but it doesn’t address the core problem of diversifying a single large, appreciated stock without triggering gains.

Exchange funds solve that by:

- Allowing you to contribute your concentrated stock in exchange for shares in a diversified fund, achieving instant diversification without realizing capital gains.

- Deferring your gains indefinitely, while allowing your capital to continue working for you.

Direct Indexing vs. Exchange Funds: Strategic Insights

Direct indexing and exchange funds both offer meaningful diversification and sophisticated tax advantages, but cater to different investor needs and time horizons:

Combining Direct Indexing with Exchange Funds: An Optimal Approach

A savvy investor might strategically combine these approaches—using direct indexing to tailor smaller, actively managed portfolios for personalized control and tax-loss harvesting, while employing exchange funds like Cache to efficiently and strategically diversify substantial, concentrated positions over the long term, thereby avoiding significant upfront tax consequences.

The Cache Advantage

Cache Exchange Funds offers sophisticated investors a powerful solution to diversification, one that was previously not widely accessible. For the first time, Cache has made exchange funds available to more investors by lowering minimums to $100K, broadening access to accredited investors, and offering a range of choices, including Nasdaq-100 and S&P 500.

Summary

Direct indexing and exchange funds aren’t competitors—they’re complementary tools for sophisticated investors. Direct indexing helps you optimize broad portfolios year after year. Cache Exchange Funds can help unlock diversification from concentrated stock positions without triggering gains. Used together, they provide the flexibility to harvest in the short term while securing long-term freedom from concentration risk.

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.