The Hidden Risk in Your Portfolio, and How to Fix It

Tim Kochis, JD, CFP®

Strategic Advisor and Investor

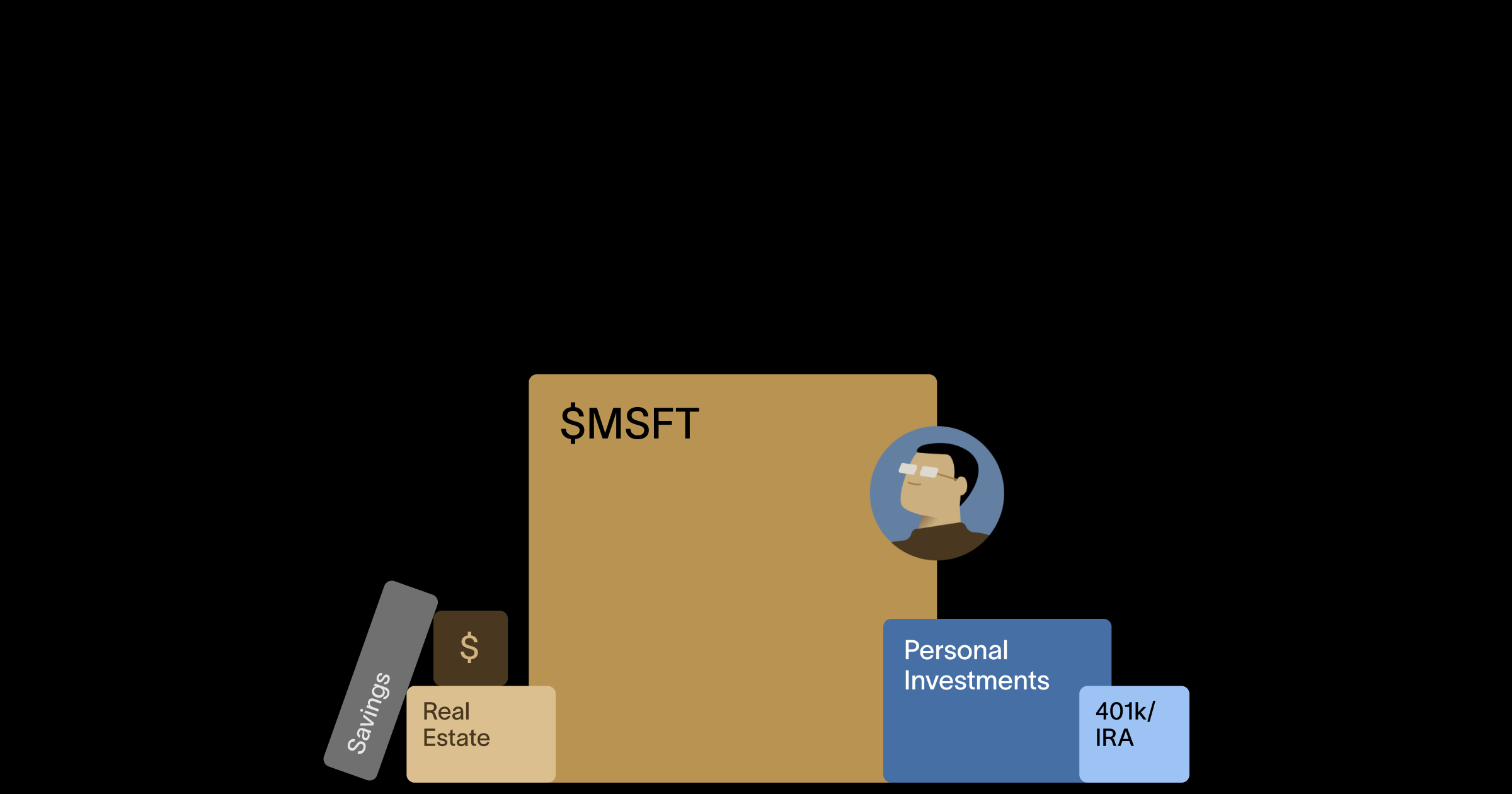

For many across the tech industry and beyond, the promise of long-term wealth is built into every equity grant. Yet the reality of that promise requires patience and faith, as the wait can stretch for years, shaped by unpredictable markets and valuations. You might be living that reality now, with millions tied to the company you helped build.

It’s an enviable position, but one that carries a quiet risk. When a single stock dominates your financial life, the potential reward is enormous, yet the downside can be devastating. That imbalance is what we call concentration risk.

Understanding Concentration Risk

If you’ve worked for a successful company, it’s almost impossible not to accumulate significant stock through RSUs, options, or grants. The question is: how much is too much? Ten percent of your portfolio? Fifty? Ninety? There’s no universal answer. It depends on your total wealth, your goals, and how much uncertainty you can tolerate.

Concentration builds quietly. Roma's household ended up holding positions across six major tech companies before she addressed it. Here's how Roma finally made the move.

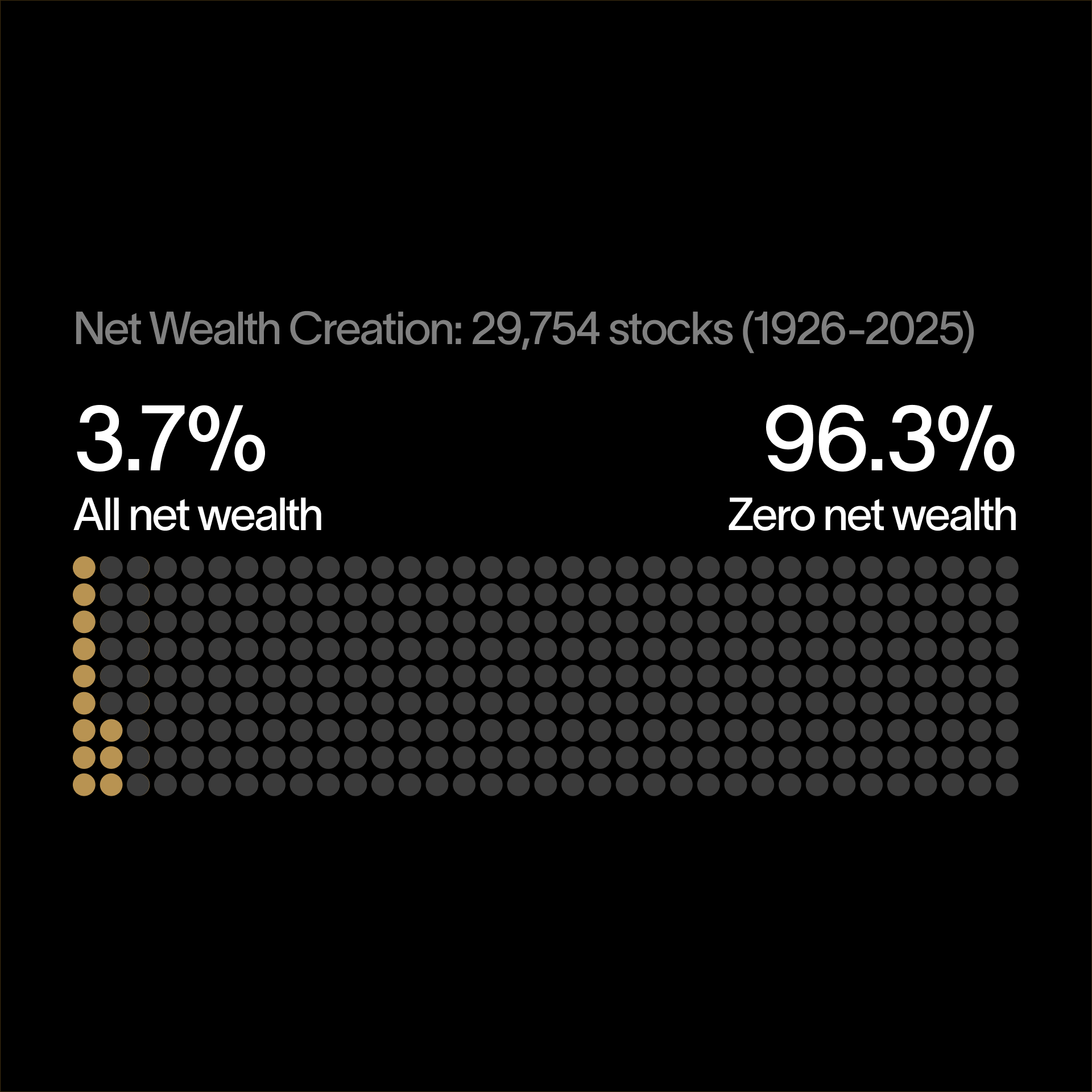

It’s easy to focus on the upside, especially when your company keeps growing. But real wealth management isn’t about optimism. It’s about protecting yourself from what you can’t predict or control. History offers plenty of examples of once-great companies that lost seventy, eighty, even ninety percent of their value and never recovered. By contrast, investors who held an S&P 500 index fund through the 2008 crisis saw losses of roughly half, but regained everything within three years and went on to earn multiples since.

That contrast illustrates a simple truth: diversification works. Holding a single stock can feel exciting and personal, but holding many makes you resilient.

Why Diversification Matters

The market doesn’t pay extra for taking unnecessary risk. A concentrated position exposes you to what professionals call “uncompensated risk:” the chance of major loss without any offsetting return.

Diversifying doesn’t mean owning hundreds of companies. Holding as few as ten to twelve uncorrelated stocks, or a single broad ETF, gets you most of the benefit. What matters is that those holdings don’t all move in the same direction at the same time.

You might think, “But I know my company better than anyone.” Maybe you do. Still, your stock’s price reflects the collective judgment of millions of investors around the world. It’s a bold bet to assume you can outguess all of them or anticipate the unexpected events that arise out of nowhere. Submitting to the wisdom of the market isn’t defeat, it’s discipline.

Can You Afford the Risk?

Some people can afford concentration risk. Most cannot. It depends on how your total resources compare to the cost of your goals. If you have more than you’ll ever need, you’re rich in any definition that matters. If your resources fall short of what it will take to fund your future, you’re vulnerable, no matter how many zeroes are on your brokerage statement.

Even if this is your first windfall, be careful. Goals evolve, families grow, priorities shift, and opportunities expand. The balance you strike today between risk and reward will shape how much flexibility you have later. Managing concentration risk doesn’t mean selling everything. It means making sure one company’s fate doesn’t define your future.

The Role of Taxes

If diversification were tax-free, most people would do it immediately. But taxes complicate the equation. Selling appreciated stock can trigger federal and state capital gains of up to forty percent, and that number can feel painful, especially when the appreciation represents years of effort.

Still, perspective helps. When you step back, the tax cost often looks more like a one-time sales tax on a life-changing outcome than a penalty. Paying some tax to protect your wealth is rarely a bad trade. Refusing to diversify because of it can be far costlier in the long run.

Smart Ways to Reduce the Burden

Fortunately, there are ways to reduce or transfer that tax burden. Two of the most powerful are gifting and charitable giving.

- Gift stock to family members in lower tax brackets, transferring both the asset and its future appreciation out of your estate.

- Donate appreciated shares to a charity or donor-advised fund. You’ll receive a deduction for the full market value, and the charity can sell tax-free.

These approaches don’t solve every situation, but they can significantly lighten the load.

What Else You Can Do

Beyond gifting, you have several tools for managing what remains of your concentrated position:

- Stop buying more. If concentration is already a problem, don’t make it worse.

- Sell strategically. For many investors, selling gradually over time is the fastest, simplest fix.

- Leverage to diversify. Borrow against your shares to buy other assets. Used carefully, this can help reduce risk through diversification, but treat it as a precision tool, not a shortcut.

- Hedge with options. Writing covered calls or buying puts can help manage volatility.

- Use collars. A collar limits both downside and upside within a set range, often at little to no net cost.

Each of these approaches has trade-offs, and none is one-size-fits-all. But combined thoughtfully, they can help you preserve opportunity while reducing exposure.

Exchange Funds: The Original Diversification Tool

Exchange funds have existed for decades as one of the most tax-efficient ways to manage concentration. You contribute your stock to a shared fund alongside other investors contributing different stocks. Under IRS rules, the fund must hold at least twenty percent in illiquid assets, such as real estate, to qualify for tax deferral. After seven years, you receive a diversified basket of stocks, carrying your original cost basis forward.

They were once reserved for those with private banking access and multimillion-dollar minimums. Cache changed that.

It’s an elegant idea, but traditional exchange funds come with drawbacks. Minimums are high, fees can be steep, and portfolios often include stocks from similar sectors, which limits diversification. The seven-year holding period is also fixed by law, which limits flexibility.

Cache - A Better Way Forward

That’s why I’ve begun working with the team at Cache, who have rebuilt the exchange-fund model for modern investors. Cache opens the door to this strategy for far more people, with minimums as low as $100,000, broad index-level diversification, and transparent pricing. Each fund is built to mirror the S&P 500 or Nasdaq-100 with roughly 99 percent correlation, giving you true market exposure from day one.

You still get the same tax deferral and seven-year horizon, but now with lower fees, greater transparency, and simpler access. It’s not the right tool for everyone, but for many, it’s a thoughtful way to reduce risk without triggering tax.

The Bottom Line

Concentration risk is a good problem to have, but it’s still a problem. You’ve worked hard to build your wealth. Now the challenge is protecting it—without giving up opportunity.

- Diversify where you can.

- Be thoughtful about taxes.

- And make sure the company that built your wealth doesn’t define it.

That’s how you turn success into security.

--

Correlation measures how closely an investment’s returns move in relation to a benchmark. It’s a backward-looking statistic used to assess how well an exchange fund has tracked its benchmark over a given period. Correlation is measured over a 1-month period in arrears. Information is current as of Octover 27th, 2025, and is not updated.

Cache Exchange Funds are alternative investments available only to eligible investors. They are designed for long-term investors willing to accept limited liquidity and higher fees than traditional investments. Exchange funds defer but do not eliminate capital gains taxes. Diversification does not guarantee profit or protect against loss. All investments carry risk, including loss of principal.

Cache Financials Inc. | 95 Third St, Floor 2, San Francisco, CA 94103.

The Cache Exchange Fund can help.

Make better decisions for managing your large stock positions.

Sign up to receive all our insights and data.